Key attention points from this quarter:

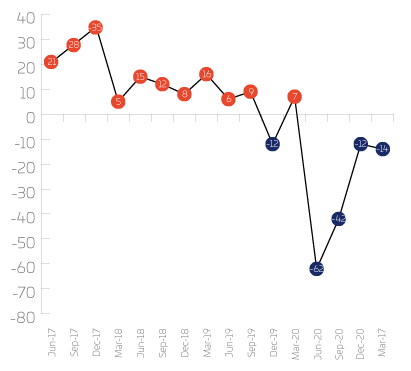

- Order intake and exports slip back by -5% and -11% from last quarter

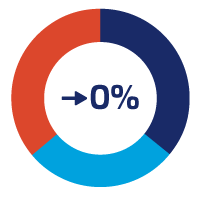

- Output volume increases 2 points to a balance of net zero

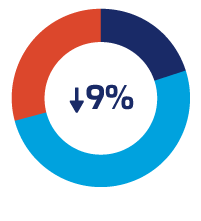

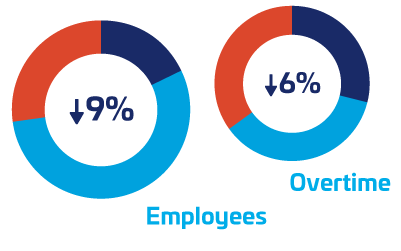

- Companies staffing levels continues to slow its rate of decline, standing at -9% this quarter, an improvement of 8%

- Confidence overall holds flat at -9%, 29% of respondents remain negative reinforcing sectors with lowest demand forecasting absence of visible recovery

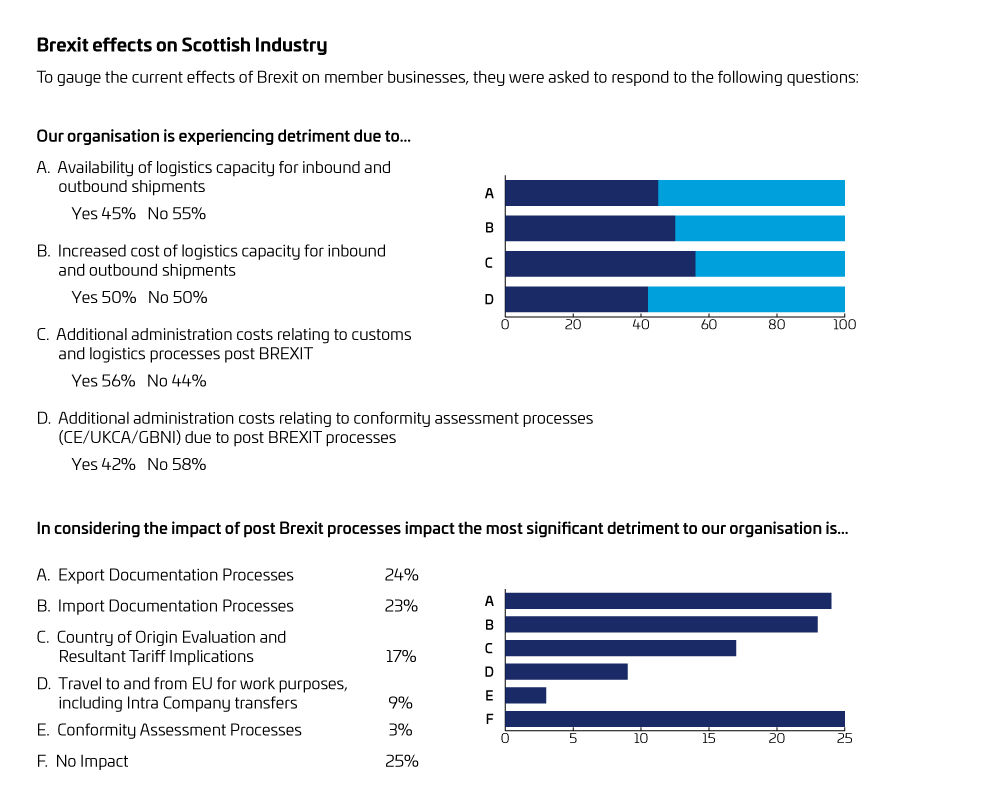

- Only one in four companies (25%) report ‘No Impact’ from the impact of post Brexit processes, with export documentation burden the most common impact

- More than half (56%) of responding companies are experiencing detriment due to additional customs and logistics administration costs post-Brexit

The data in this Review were acquired by a survey of Scottish Engineering’s members and certain other manufacturing companies.

36% of members responded

Companies are described as:

Small (<100 employees), Medium (100–500) and Large (>500)

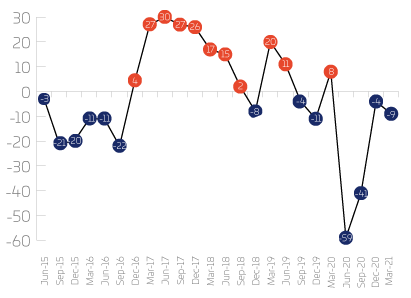

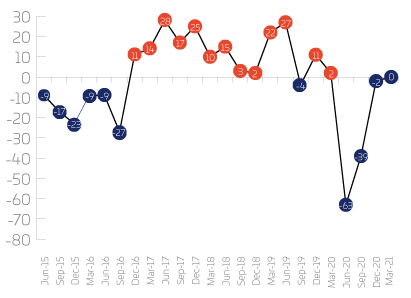

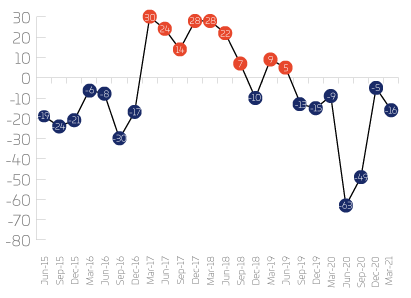

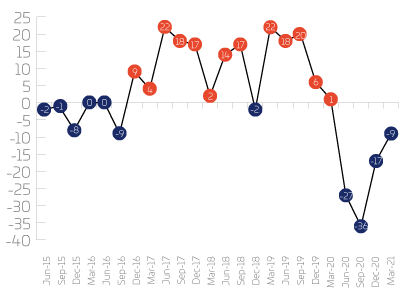

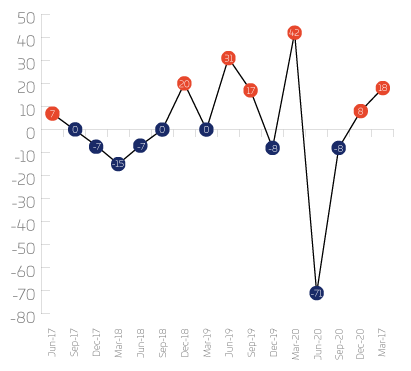

Output volume, and staffing have improved slightly since last quarter, whilst order intake and exports have fallen – all remain negative. Output volume and staffing have improved by 2 and 8 percentage points respectively; order intake and exports are down by 5 and 11 percentage points.

Order intake

Output volume

Exports

Staffing

Net | Up | Same | Down | |

UK Orders | -15% | 28% | 29% | 43% |

Small companies | -18% | 27% | 28% | 45% |

Medium | -4% | 31% | 34% | 35% |

Large companies | -33% | 17% | 33% | 50% |

Machine shops | -30% | 30% | 10% | 60% |

Mechanical | -7% | 30% | 33% | 37% |

Metal | -50% | 25% | 0% | 75% |

Non-metal | -29% | 29% | 14% | 57% |

Fabricators | 18% | 36% | 46% | 18% |

Electronics | -29% | 14% | 43% | 43% |

UK orders are negative, with the balance of change at -15%. All sizes of company are reporting decreases. Across the sectors fabricators are reporting increases, but all other sectors are reporting a downturn.

Net | Up | Same | Down | |

Export Orders | -16% | 23% | 38% | 39% |

Small companies | -18% | 23% | 36% | 41% |

Medium companies | -13% | 21% | 46% | 33% |

Large companies | -17% | 33% | 17% | 50% |

Machine shops | -50% | 17% | 16% | 67% |

Mechanical | 0% | 31% | 38% | 31% |

Metal | -67% | 0% | 33% | 67% |

Non-metal | 0% | 29% | 42% | 29% |

Fabricators | -25% | 0% | 75% | 25% |

Electronics | 0% | 50% | 0% | 50% |

Export orders are negative, with the balance of change at -16%. All sizes of company are reporting decreases, the balance of change is -18% for small companies, -13% for medium companies, and -17% for large companies. In the sectors the balance of change is -50% for machine shops, -67% for metal manufacturing, and -25% for fabricators; mechanical equipment, non-metal products and electronics are reporting equal numbers of increases and decreases.

Net | Up | Same | Down | |

Optimism | -9% | 20% | 51% | 29% |

Small companies | -13% | 19% | 48% | 33% |

Medium companies | 0% | 21% | 58% | 21% |

Large companies | 0% | 17% | 66% | 17% |

Machine shops | -40% | 10% | 40% | 50% |

Mechanical equipment | -6% | 16% | 62% | 22% |

Metal manufacturing | -13% | 25% | 37% | 38% |

Non-metal products | 0% | 29% | 42% | 29% |

Fabricators | 0% | 36% | 28% | 36% |

Electronics | 57% | 71% | 15% | 14% |

Optimism has remained the same as last quarter, at -9%. Small companies are reporting decreases, whilst medium and large companies are reporting equal numbers of increases and decreases. Across the sectors machine shops, mechanical equipment and metal manufacturing are reporting decreases, electronics are reporting increases and non-metal products and fabricators are reporting equal numbers of increases and decreases.

Net | Up | Same | Down | |

Output volume | 0% | 36% | 28% | 36% |

Small companies | -7% | 34% | 24% | 42% |

Medium | 15% | 37% | 41% | 22% |

Large companies | 17% | 50% | 17% | 33% |

Machine shops | -30% | 10% | 50% | 40% |

Mechanical | 9% | 44% | 22% | 34% |

Metal | -25% | 25% | 25% | 50% |

Non-metal | -29% | 29% | 14% | 57% |

Fabricators | 9% | 36% | 37% | 27% |

Electronics | 57% | 71% | 15% | 14% |

Output volume has improved 2 percentage points since last quarter and the balance of change is now 0, small companies remain negative whilst medium and large sized companies are reporting increases of 15 and 17 percentage points respectively. Within the sectors machine shops, metal manufacturing and non-metal products are reporting decreases; and mechanical equipment, fabricators and electronics are reporting increases.

Net | Up | Same | Down | |

Staffing | -9% | 18% | 55% | 27% |

Small companies | -16% | 15% | 54% | 31% |

Medium | -4% | 19% | 59% | 22% |

Large companies | 50% | 50% | 50% | 0% |

Machine shops | -30% | 0% | 70% | 30% |

Mechanical | -6% | 25% | 44% | 31% |

Metal | -63% | 0% | 37% | 63% |

Non-metal | -43% | 0% | 57% | 43% |

Fabricators | 27% | 36% | 55% | 9% |

Electronics | -14% | 14% | 57% | 29% |

Employees

Employee numbers are positive for large companies, but small and medium companies are reporting decreases. Fabricators are the only sector reporting an increase in employees.

Net | Up | Same | Down | |

Overtime | -6% | 29% | 36% | 35% |

Small companies | -16% | 21% | 41% | 38% |

Medium companies | 11% | 41% | 29% | 30% |

Large companies | 17% | 50% | 17% | 33% |

Overtime working has picked up, medium and large companies are reporting increases, but it is still reduced for small companies.

Net | Up | Same | Down | |

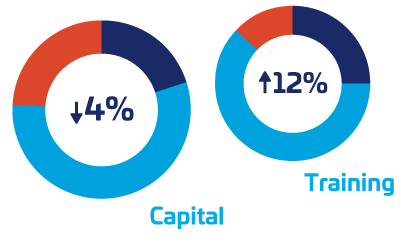

Investment | -4% | 20% | 56% | 24% |

Small companies | -8% | 19% | 54% | 27% |

Medium | 7% | 25% | 57% | 18% |

Large companies | -17% | 0% | 83% | 17% |

Machine shops | -60% | 0% | 40% | 60% |

Mechanical | -9% | 9% | 72% | 19% |

Metal | -38% | 13% | 37% | 50% |

Non-metal | 14% | 29% | 57% | 14% |

Fabricators | 10% | 40% | 30% | 30% |

Electronics | 17% | 17% | 83% | 0% |

Investment

Capital investment plans have dipped since last quarter, with small and large sizes of company now reporting negative net returns. Within the sectors non-metal products, fabricators, and electronics are reporting positive net returns, and machine shops, mechanical equipment and metal manufacturing are reporting negative net returns.

Net | Up | Same | Down | |

Training Investment | 12% | 25% | 62% | 13% |

Small companies | 9% | 24% | 61% | 15% |

Medium companies | 14% | 25% | 64% | 11% |

Large companies | 33% | 3% | 67% | 0% |

All sizes of company are reporting positive figures for training investment.

Capacity Utilisation

Capacity utilisation has fallen 2 percentage points since last quarter and remains negative at -14%.

Fabricators

Order Intake Total Fabricator order intake is positive for the second consecutive quarter.

Forecast

The last twelve months have been extremely challenging for our sector, but forecasts for the next three months look to improve slightly, although some measures remain negative. In general, overall orders, UK orders and output volume are forecast to recover slightly, but export orders remain negative at -3%. All sizes of company are forecasting positive figures for UK order intake, export prices, output volume and employee numbers. Small and medium companies are forecasting negative figures for export orders, and medium companies are expecting UK prices to be negative.

Metal manufacturing, non-metal products, fabricators and mechanical equipment are forecasting an increase in U.K. order intake, whilst electronics and machine shops are forecasting a decrease. Mechanical equipment is the only sector forecasting an increase in export orders. The forecasts for UK pricing are positive or neutral. Metal manufacturing and electronics are forecasting a decrease in export prices, whilst non-metal products, fabricators and mechanical equipment are forecasting an increase. Forecasts for output are positive from non-metal products, fabricators and mechanical equipment, but other sectors are neutral or anticipating a decrease. Metal manufacturing and machine shops are anticipating decreases in employee numbers, whilst all other sectors are forecasting increases.

| Net | Up | Same | Down | |

Orders | 15% | 39% | 37% | 24% |

UK Orders | 13% | 36% | 42% | 22% |

Export Orders | -3% | 26% | 45% | 29% |

Output Volume | 9% | 35% | 38% | 26% |

Balance of change %

| Order Intake UK | Orders Export | Prices UK | Prices Export | Output Volume | Employees | |

|---|---|---|---|---|---|---|

| Small | 9 | -7 | 24 | 16 | 9 | 10 |

| Medium | 19 | -4 | -8 | 8 | 0 | 18 |

| Large | 33 | 33 | 0 | 17 | 50 | 67 |

| Metal Manufacturing | 25 | 0 | 0 | -33 | 0 | -13 |

| Non-Metal Products | 14 | -29 | 43 | 43 | 14 | 14 |

| Electronics | -29 | -17 | 14 | -17 | -29 | 29 |

| Fabricators | 9 | 0 | 18 | 50 | 10 | 18 |

| Machine Shops | -10 | -17 | 10 | 0 | -10 | -10 |

| Mechanical Equipment | 30 | 18 | 23 | 21 | 28 | 16 |