Overall order intake – and especially exports - falls further negative along with output volume, and our long run of positive optimism evaporates too. An intent to increase staffing ends its four year run in this survey return too. There is little good news to point to, as whilst forecasts are generally positive, the last quarter’s actual orders did not match the preceding forecast, and so caution is perhaps required here too.

Key attention points from this quarter:

- Overall order intake amongst members fell negative to a net -8% with export orders again the stronger driver for reduction

- Output volume also dipped to a net of -8%, negative for the second quarter in a row

- For the coming three months, members forecast a net increase of 10% of businesses having increased orders, with output forecast to remain at a net negative -3% increase in the same period

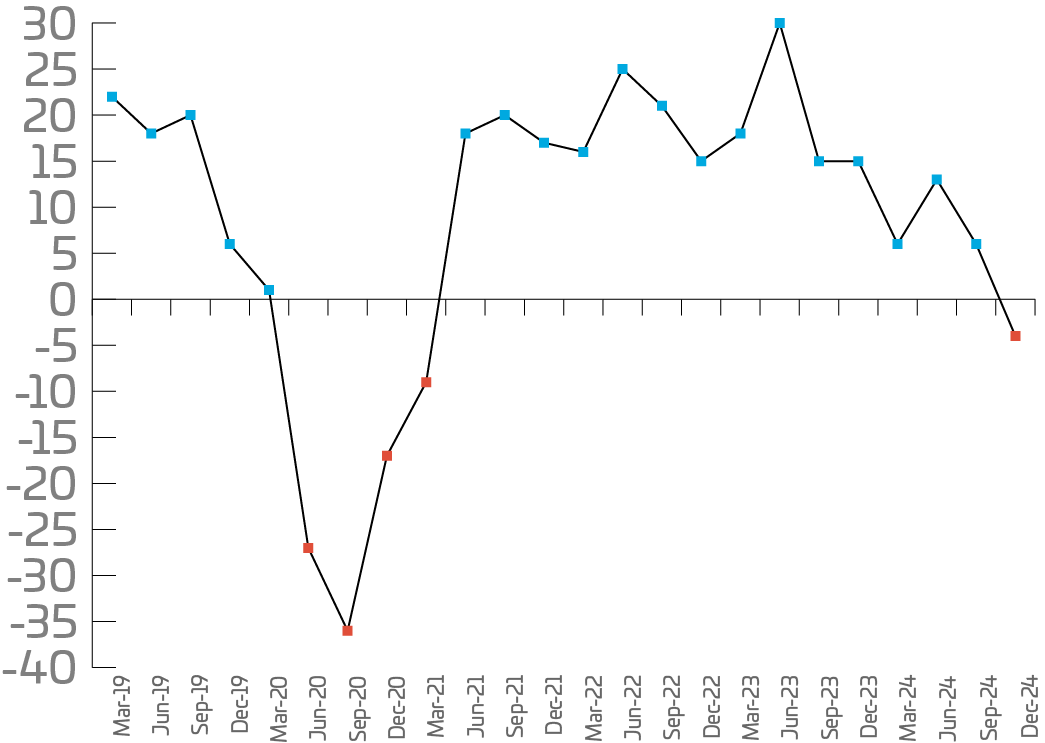

- Optimism falls negative for the first time in almost four years with a net -19% of our survey respondents reflecting a negative outlook

The data in this Review was acquired by a survey of Scottish Engineering’s members and certain other manufacturing companies.

31% of members responded

Companies are described as:

Small (<100 employees), Medium (100–500) and Large (>500)

Annual trends

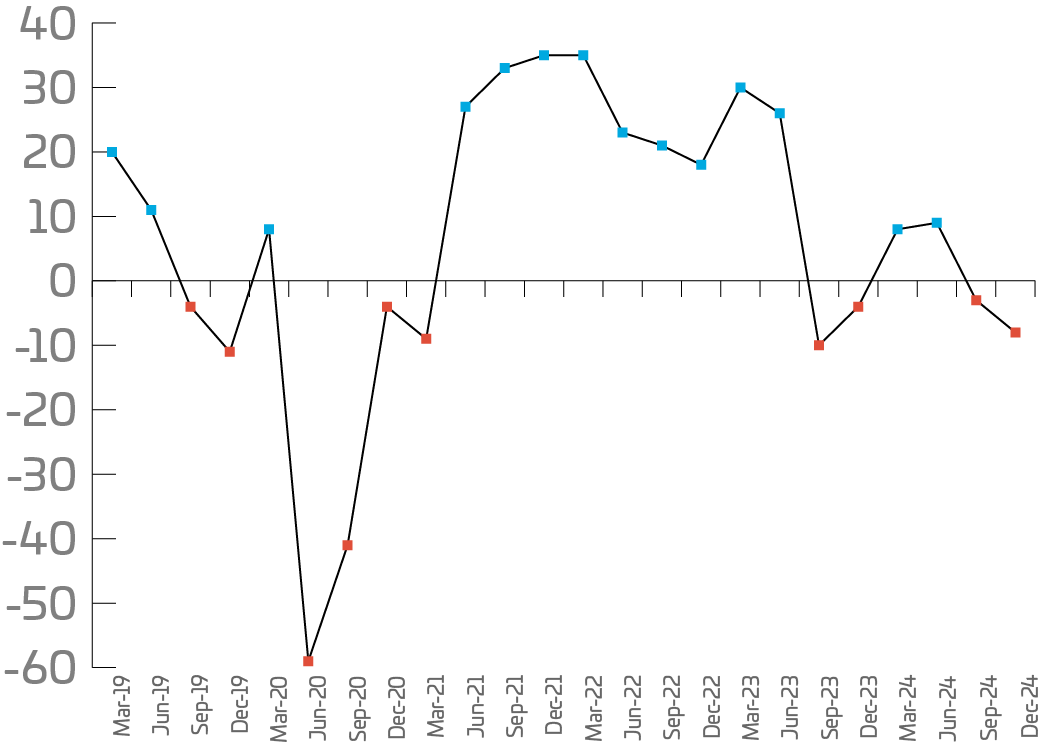

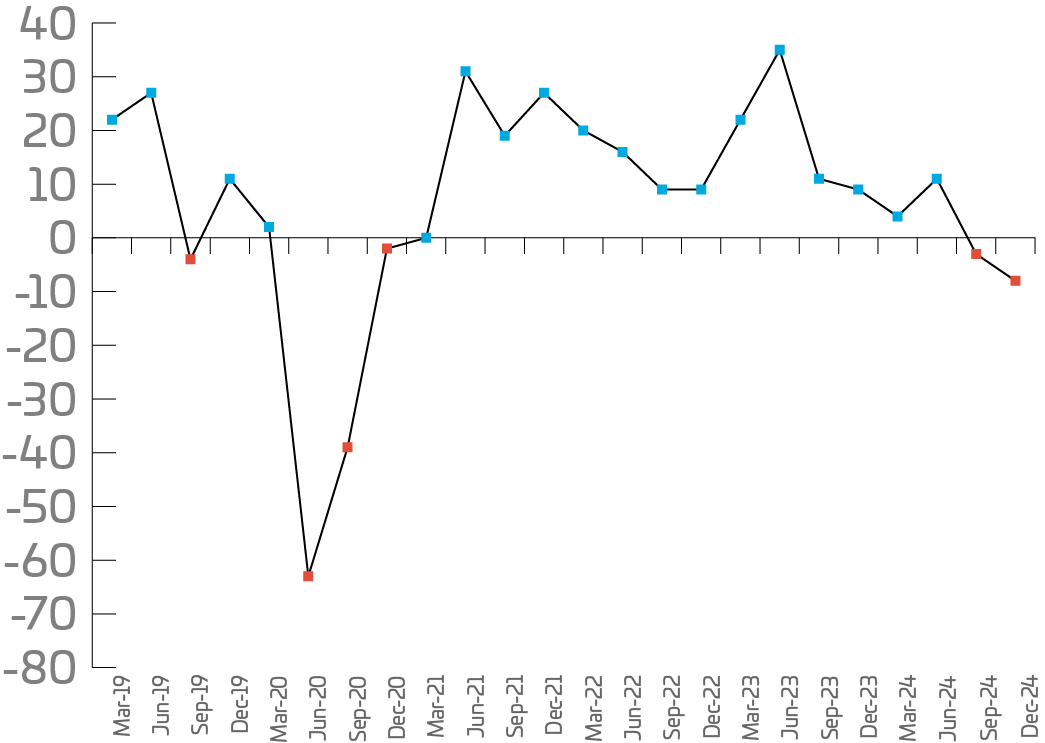

The fourth quarter indicates a decline in order intake of -8% on the previous quarter, together with output volume and exports returning similar negative movement from last quarter of -8% and -19% respectively. Staffing has shown positive demand over the last 15 consecutive quarters, however, this quarter records decline by -4%. Capacity utilisation also indicates a negative movement of -12%, after being positive for the last 14 consecutive reports.

Order intake

Output volume

Exports

Staffing

UK Orders

Net | Up | Same | Down |

-12% | 27% | 34% | 39% |

UK orders record a third consecutive decrease, to a net -12%. Small and medium companies have impacted this decline (-23% and -4%), with larger companies showing positivity at +50%. Although Precision Engineering and Fabricators have equal positive and negative returns this quarter, they have improved from -30% to 0% and -8 to 0% consecutively. Manufacturing and Electrical & Electronics are showing a decline (-25% and -11%), all moving from equal positive and negative returns last quarter (0%). Metal Products and Plant & Machinery show negative returns this quarter, (-67% and –16%). Plant & Machinery are reporting negative returns at the same level as last quarter (-17%). Metal Products also report negative, with a slight downward trajectory in comparison to last quarter (from -50% to -67%).

Companies | Net | Up | Same | Down |

| Small | -23% | 25% | 27% | 48% |

Medium | -4% | 26% | 44% | 30% |

Large | 50% | 50% | 50% | 0% |

Sectors |

|

|

|

|

Manufacturing | -25% | 18% | 39% | 43% |

Plant & Machinery | -16% | 17% | 50% | 33% |

Metal | -67% | 0% | 33% | 67% |

Precision | 0% | 40% | 20% | 40% |

Fabricators | 0% | 31% | 38% | 31% |

Electrical & Electronics | -11% | 22% | 45% | 33% |

Export Orders

Net | Up | Same | Down |

-19% | 22% | 37% | 41% |

Export orders have fallen to a net -19%, a decline from last quarter of -15%. All sizes and companies have driven the increase with larger companies most impacted, recording a movement of -43% (-20% last quarter). All sizes of companies have seen a slight downward trajectory (small -18% to -19%) and medium (-8% to -13%). Plant & Machinery are reporting positive returns of +34%, an improvement after recording equal and positive returns last quarter. Although Metal Products and Manufacturing have reported decreased export orders at –34% and -20% respectively, there is an upward trajectory (-50% and -21% last quarter). Precision Engineering and Fabricators are reporting negative returns of –37% and -20% sequentially, a fall (-25% and 0% respectively.)

Companies | Net | Up | Same | Down |

Small | -19% | 21% | 39% | 40% |

Medium | -13% | 25% | 37% | 38% |

Large | -43% | 14% | 29% | 57% |

Sectors |

|

|

|

|

Manufacturing | -20% | 24% | 32% | 44% |

Plant & Machinery | 34% | 56% | 22% | 22% |

Metal | -34% | 33% | 0% | 67% |

Precision | -37% | 13% | 37% | 50% |

Fabricators | -20% | 0% | 80% | 20% |

Electrical & Electronics | -56% | 0% | 44% | 56% |

Optimism

Net | Up | Same | Down |

-13% | 17% | 53% | 30% |

Optimism, for the first time in almost four years has fallen below the line with a net -13% for all companies. Medium companies remain positive for a 4th consecutive quarter at +3%, a decline for smaller companies at -21%, with larger companies recording equal positive and negative returns (0%). Plant & Machinery remain positive in their outlook at +7%. Manufacturing have moved from positive returns last quarter to negative (-11% from +11%). Metal Products and Precision engineering have moved from recording equal positive and negative returns last quarter to -67% and -40% respectively. Fabricators and Electrical & Electronics are both reporting negative returns, -8% and -33% respectively.

Companies | Net | Up | Same | Down |

Small | -21% | 16% | 47% | 37% |

Medium | 3% | 17% | 69% | 14% |

Large | 0% | 22% | 56% | 22% |

Sectors |

|

|

|

|

Manufacturing | -11% | 14% | 61% | 25% |

Plant & Machinery | 7% | 38% | 31% | 31% |

Metal | -67% | 0% | 33% | 67% |

Precision Engineering | -40% | 0% | 60% | 40% |

Fabricators | -8% | 21% | 50% | 29% |

Electrical & Electronics | -33% | 11% | 45% | 44% |

Output Volume

Net | Up | Same | Down |

-9% | 28% | 35% | 37% |

Output volume, for the first time since 2020 had seen a decline of -3% overall, declining further this quarter to –9%. Larger companies remain positive at +11%, with smaller and medium companies recording negative returns of -13% and -4% consecutively. Manufacturing and Plant & Machinery are showing equal positive and negative returns on last quarter. Metal Products, Electrical & Electronics Precision Engineering, and Fabricators are showing negative returns (-67%, -56%, -40% and -21%), an improvement however, for Fabricators from last quarter (-33%). Metal Products and Precision Engineering are reporting largest decline from equal positive and negative returns from last quarter.

Companies | Net | Up | Same | Down |

Small | -13% | 29% | 29% | 42% |

Medium | -4% | 25% | 46% | 29% |

Large | 11% | 33% | 45% | 22% |

Sectors |

|

|

|

|

Manufacturing | 0% | 39% | 22% | 39% |

Plant & Machinery | 0% | 17% | 66% | 17% |

Metal | -67% | 0% | 33% | 67% |

Precision | -40% | 20% | 20% | 60% |

Fabricators | -21% | 21% | 36% | 43% |

Electrical & Electronics | -56% | 11% | 22% | 67% |

Staffing

Net | Up | Same | Down |

-4% | 23% | 50% | 27% |

Employee numbers are static for larger companies (0%) with equal positive and negative returns this quarter but a decline for small and medium companies (-4% and -3% respectively). Metal Products show a decline of -67% (-25% last quarter) followed by Manufacturing at -28% (-15% last quarter) and Fabricators -14% (0% last quarter), all on a downward trajectory on last quarter. Electrical & Electronics equal positive and negatives returns this quarter (+30% last quarter). Precision Engineering and Plant & Machinery show positivity (+30% and +15%), an upward trajectory on last quarter (+20% and +8%).

Companies | Net | Up | Same | Down |

Small | -4% | 21% | 53% | 26% |

Medium | -3% | 28% | 41% | 31% |

Large | 0% | 22% | 56% | 22% |

Sectors |

|

|

|

|

Manufacturing | -28% | 11% | 50% | 39% |

Plant & Machinery | 15% | 38% | 39% | 23% |

Metal | -67% | 0% | 33% | 67% |

Precision | 30% | 40% | 50% | 10% |

Fabricators | -14% | 14% | 57% | 29% |

Electrical & Electronics | 0% | 33% | 34% | 33% |

Overtime

Overtime has seen a slight decline this quarter with smaller companies reporting the largest decrease of –9% (-8% last quarter). Medium and larger companies show equal and positive returns this quarter reflecting decreases in both UK and Export orders.

Companies | Net | Up | Same | Down |

-6% | 23% | 48% | 29% | |

Small | -9% | 22% | 47% | 31% |

Medium | 0% | 24% | 52% | 24% |

Large | 0% | 33% | 34% | 33% |

Investment

Net | Up | Same | Down |

3% | 24% | 55% | 21% |

Capital investment plans remain positive overall at +3%: small companies are down –3% on last quarter, medium companies are +18% and large companies are reporting equal positive and negative returns Metal products are, for the second quarter running report equal positive and negative returns on last quarter. Plant & Machinery indicate the highest level of investment, an improvement of +25%, followed by Electrical & Electronics (+11%). Precision Engineering and Fabricators both show negative returns at -10% and -7% consecutively with Manufacturing showing both equal positive and negative returns (0%).

Companies | Net | Up | Same | Down |

Small | -3% | 22% | 53% | 25% |

Medium | 18% | 32% | 54% | 14% |

Large | 0% | 11% | 78% | 11% |

Sectors |

|

|

|

|

Manufacturing | 0% | 19% | 62% | 19% |

Plant & Machinery | 25% | 42% | 41% | 17% |

Metal | 0% | 33% | 34% | 33% |

Precision | -10% | 20% | 50% | 30% |

Fabricators | -7% | 14% | 65% | 21% |

Electrical & Electronics | 11% | 33% | 45% | 22% |

Training Investment

Although members continue to struggle with their skill challenges across industry, all sizes of companies are reporting increased plans for training investment, with larger companies strongest with a net +44% reporting increased training plans whilst small and medium sized companies also show positivity at +6% and +27% respectively.

Companies | Net | Up | Same | Down |

15% | 25% | 65% | 10% | |

Small | 6% | 19% | 68% | 13% |

Medium | 27% | 34% | 59% | 7% |

Large | 44% | 44% | 56% | 0% |

Capacity Utilisation

Capacity Utilisation for the first time since Q1 2021, shows a negative return with a net -12% of companies reporting that capacity utilisation has fallen.

Plant & Machinery

Although Plant & Machinery are showing a decline in UK Orders, and remaining at -17% from last quarter, the outlook shows positivity overall. Export Orders has seen a large improvement moving from 0% to +33% this quarter. This matches their investment plans improving from -9% to +25%, optimism at +8% (same as last quarter), output volume improving from -42% to 0% and increase in staffing from +8% to +15% this quarter.

Forecast

Looking at the next 3 months, forecasts reflect a mixed outlook. Medium companies forecast positivity in all areas (order intake, order exports, prices UK, prices export, output volume and employees). Smaller and medium companies forecast positive plans to hire employees, both at +7%. Plant & Machinery forecast positivity overall (order intake +23%, order exports +30%, prices UK +38%, prices export +50%, output volume +15% and employees 0%) whilst Electrical & Electronics forecast it to be more challenging (order intake -22%, order exports -22%, prices UK -11%, prices export 0%, output volume -11% and employees 0%). Metal Products are also forecasting a less positive quarter with all areas showing 0% forecasts apart from order intake with a decline of -50%.

| Net | Up | Same | Down | |

Orders | 10% | 33% | 44% | 23% |

UK Orders | -2% | 23% | 52% | 25% |

Export Orders | 5% | 28% | 49% | 23% |

Output Volume | -3% | 26% | 45% | 29% |

Balance of change %

| Order Intake UK | Orders Export | Prices UK | Prices Export | Output Volume | Employees | |

|---|---|---|---|---|---|---|

| Small | -1 | 2 | 35 | 28 | -6 | 7 |

| Medium | 4 | 16 | 11 | 20 | 3 | 7 |

| Large | -25 | -14 | 0 | 0 | 0 | 0 |

| Metal Products | -50 | 0 | 0 | 0 | 0 | 0 |

| Precision Engineering | -20 | 25 | 40 | 25 | -10 | 0 |

| Electrical & Electronics | -22 | -22 | -11 | 0 | -11 | 0 |

| Fabricators | -8 | -20 | 0 | 0 | -7 | -21 |

| Manufacturing | -4 | 20 | 32 | 21 | -11 | 21 |

| Plant & Machinery | 23 | 30 | 38 | 50 | 15 | 0 |